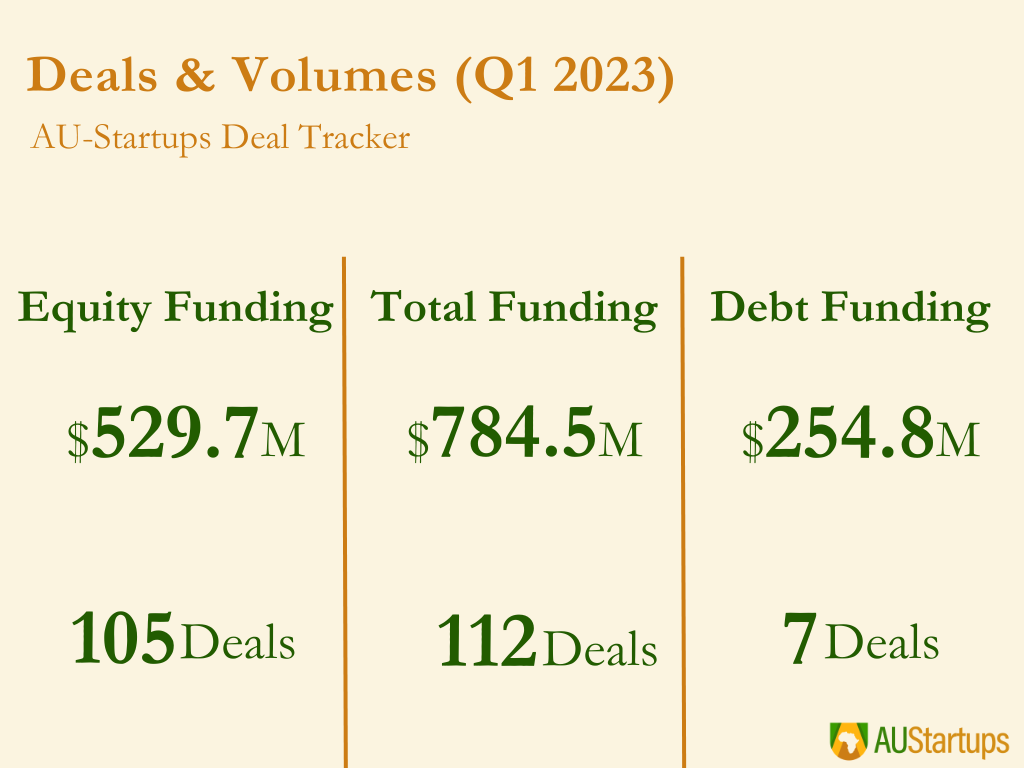

Despite the global economic downturn, Africa’s startup ecosystem is thriving and attracting investment from all over the world. In the first quarter of 2023, 209 investors invested over $784.5 million in 112 deals, representing a more than 25% increase over the previous quarter. However, this figure represents a 36% decrease from the first quarter of 2022, when African startups raised more than $1.23 billion.

While the highest number of deals occurred at the early stages (accelerator, pre-seed and seed), the largest amount of funding came from debt financing deals. This was possibly influenced by the current economic climate, with MNT-Halan and Planet42 both raising significant amounts of their funding rounds as debt.

Early stage funding was notably driven by an increase in African-focused accelerators funding their cohorts. The accelerators contributed 31% of the funding deals recorded, but only 0.6% of the funding raised. This disparity is largely due to the small ticket sizes typically associated with accelerator and pre-seed rounds.

Fintech startups received the most investments, accounting for 25% of all funding deals and raising more than 58% of all funding raised in Q1 2023. Cleantech and agtech saw increased investment, thanks to initiatives like TECA and Catalyst Fund, while Morocco surpassed South Africa and Egypt in terms of funding deals.

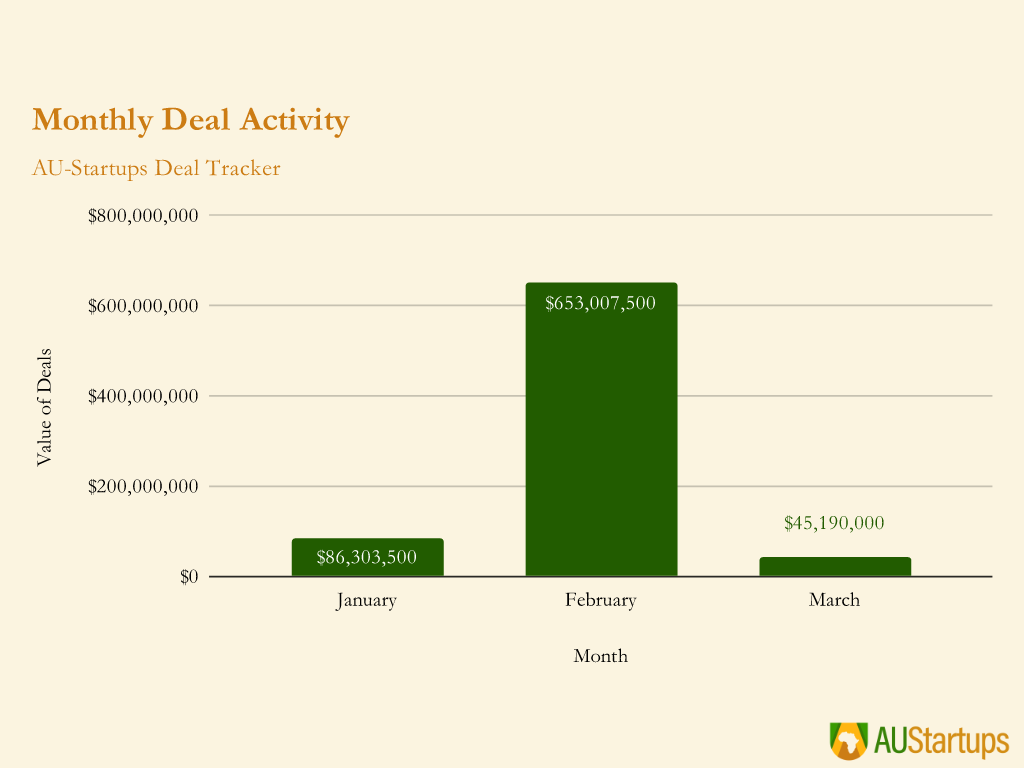

Monthly deal activity

Monthly activity by number of deals

According to our data, the number of deals closed in January and February far outnumbered those in March. This was primarily due to several accelerators announcing new cohorts during those months.

Catalyst Fund and Techstars, for example, collectively enrolled 22 startups in January, while The Baobab Network and TECA enrolled 12 in February. In contrast, March was a slow month in which no accelerator announced their cohort.

Monthly growth by value of investments

February was a particularly strong month for investment in the African startup ecosystem, with several mega-deals and big deals driving significant growth in the overall value of investments.

Notably, MNT-Halan‘s $400 million raise and Planet42‘s $100 million raise, both in February, were among the largest deals of the quarter. Additionally, Lulalend and Smile Identity’s Series B rounds, valued at $35 million and $20 million respectively, also contributed to the overall growth in investment activity in February.

It is also worth noting that the average deal size in February was $14.8 million, which was larger than all but the top two deals in January and all announced deals in March.

Geographic distribution of deals

Distribution by number of deals

The Big Four countries – Nigeria, Kenya, Egypt, and South Africa – continue to dominate in terms of deal volume, accounting for 71.4% of all deals recorded in Q1 2023. However, the number of funding deals in Morocco has steadily increased over time. In fact, Morocco surpassed Egypt and South Africa in terms of total funding deals in the first quarter. This is a positive sign that Morocco’s startup ecosystem is expanding and attracting investment, and it will be interesting to see how this trend continues in the coming quarters.

Distribution by value of investments

The Big Four countries maintained their dominance in terms of total investment value in Q1 2023, with Egypt leading the pack by raising more than twice as much funding as its nearest competitor, South Africa. In turn, the total value of funding invested in South Africa dwarfed that of all other countries combined. It is important to note, however, that this wide disparity is primarily due to the presence of two mega-rounds in Egypt and South Africa during the quarter.

If we exclude these mega-deals, South Africa would have been the clear leader in terms of deal value, followed by Egypt and the rest of the countries. Once again, we observe the rise of Morocco, which ranked 7th overall in terms of deal value. Madagascar and Ghana were outliers, with lone startups raising significant funding. WeLight, a clean energy startup from Madagascar, raised $20.5 million in debt, while Jetstream, a B2B logistics startup from Ghana, raised $13 million in a Pre-Series A round. Morocco, on the other hand, saw 12 small deals, the majority of which were seed and pre-seed rounds, with identity management startup ShareID raising the largest, a $2 million seed round.

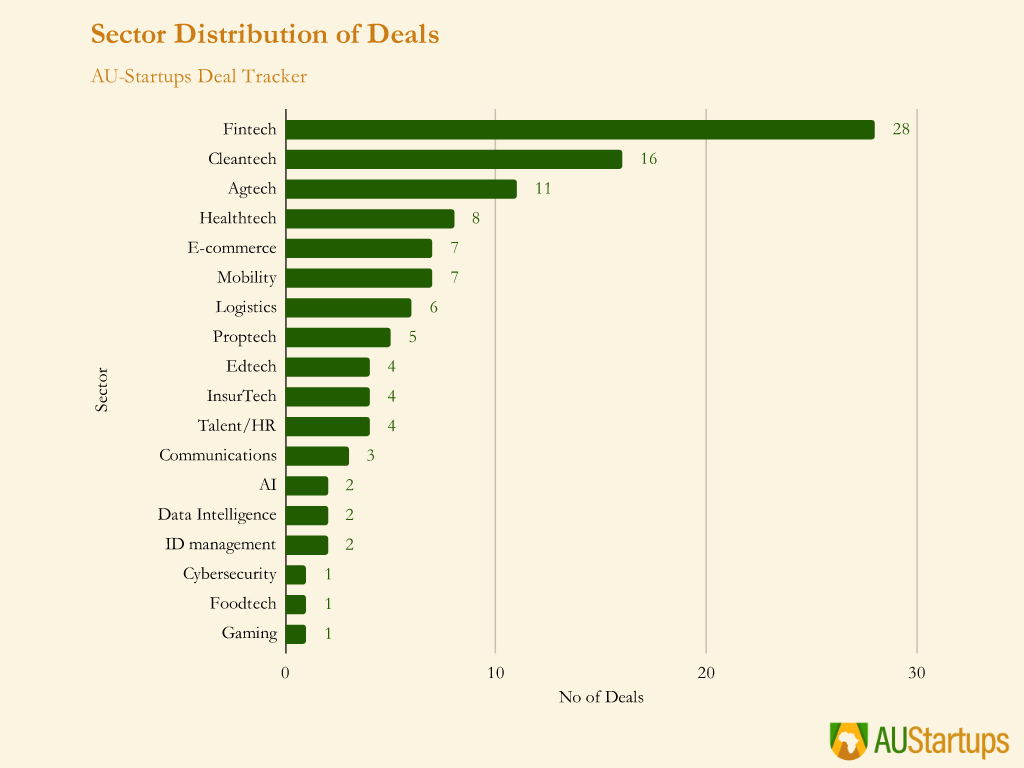

Sector distribution of deals

Distribution by number of deals

The fintech sector dominated the African startup ecosystem, accounting for 25% of all funding deals in Q1 2023. However, we observed an interesting shift, with cleantech and agtech sectors outnumbering e-commerce, logistics, and mobility in terms of funding deals.

This increase in investment in cleantech startups can be attributed to BFA Global initiatives such as TECA and Catalyst Fund, which were established to assist early-stage founders in developing technology for climate resilience and adaptation.

Distribution by value of investments

In terms of funding value, the fintech sector was the top performer, accounting for over 58% of all funding raised, up from 20% in Q4 2022, when the logistics sector led the pack. The mobility sector came in second, raising $105.7 million, thanks largely to Planet42‘s $100 million raise.

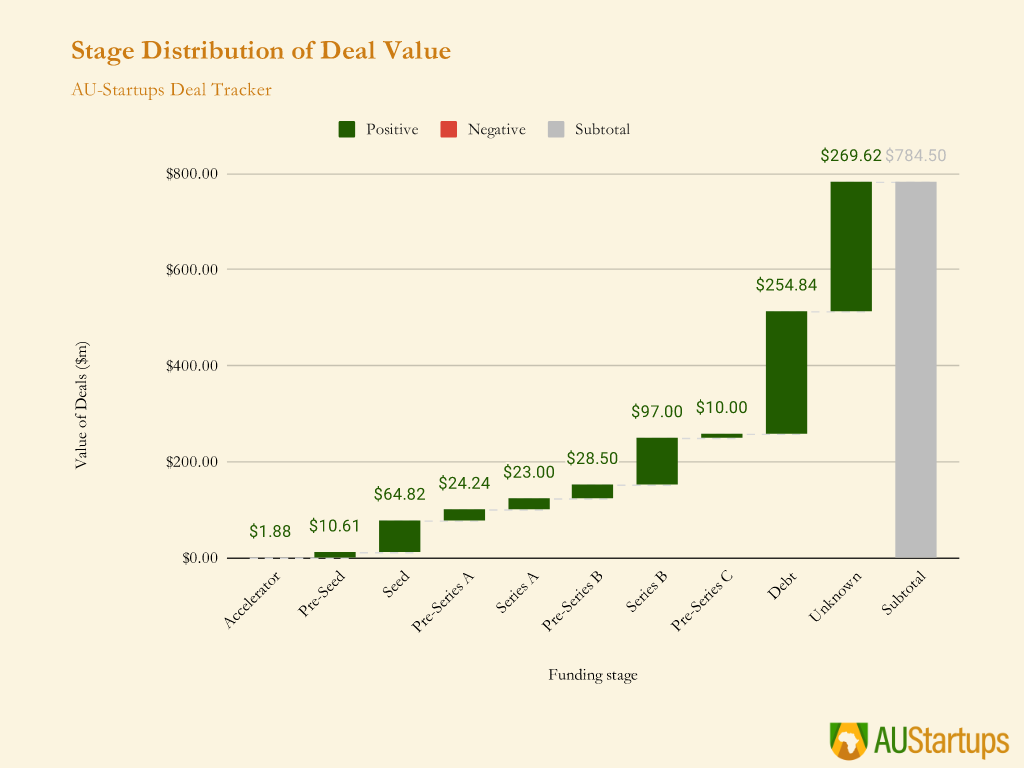

Stage distribution of deals

Distribution by number of deals

It’s encouraging to see that early stage startups received 70% of total deals in Q1 2023, indicating a thriving and active startup ecosystem. This also implies that there is a lot of entrepreneurial and innovative activity going on in the market, with investors still willing to take risks on new and unproven ideas.

Distribution by value of investments

The distribution of investments by value in Q1 2023 highlights the prominence of debt financing. This may be due to the current economic climate, in which founders are looking to unconventional sources for much needed funds.

Notably, debt financing accounted for more than 49% of the total value of fully disclosed deals, with MNT-Halan raising $140M and Planet42 raising $85M of their respective rounds through debt financing. In addition, WeLight also raised $20.5 million in debt financing.

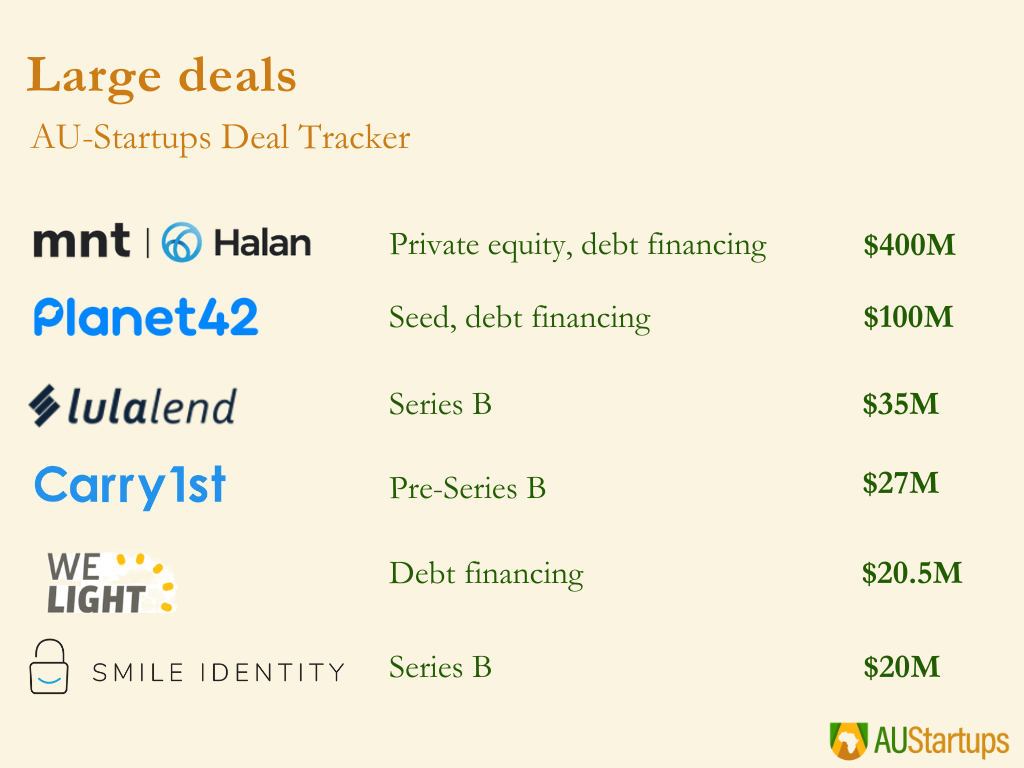

Mega-deals

In Q1 2023, there were a total of two mega-deals (≥ $100M) and four large deals (≥ $20M), which accounted for 77% of the total value of funding deals, despite representing only 5% of the number of deals raised in the quarter. These deals were primarily in the fintech and mobility sectors, with MNT-Halan’s $400M debt financing round and Planet42’s $100M seed round being the two mega-deals. Other large deals included Lulalend’s $35M Series B round and Smile Identity’s $20M Series B round.