Exploring the Venture Capital Investment Landscape for African Startups in Q3 and Q4 2022

The data* from Q3 and Q4 of 2022 reveals some interesting trends in African startup funding. The fintech sector saw a 46.2% decrease in funding between Q3 and Q4, raising questions about investor sentiment in the sector. In contrast, the logistics sector saw an impressive 89.5% increase in funding from Q3 to Q4, largely due to a mega deal from Yassir. The mobility sector also saw significant growth, with a 3,857% increase in funding between Q3 and Q4, thanks to Moove’s two big deals. E-commerce, on the other hand, experienced a 37.6% decrease in funding QoQ.

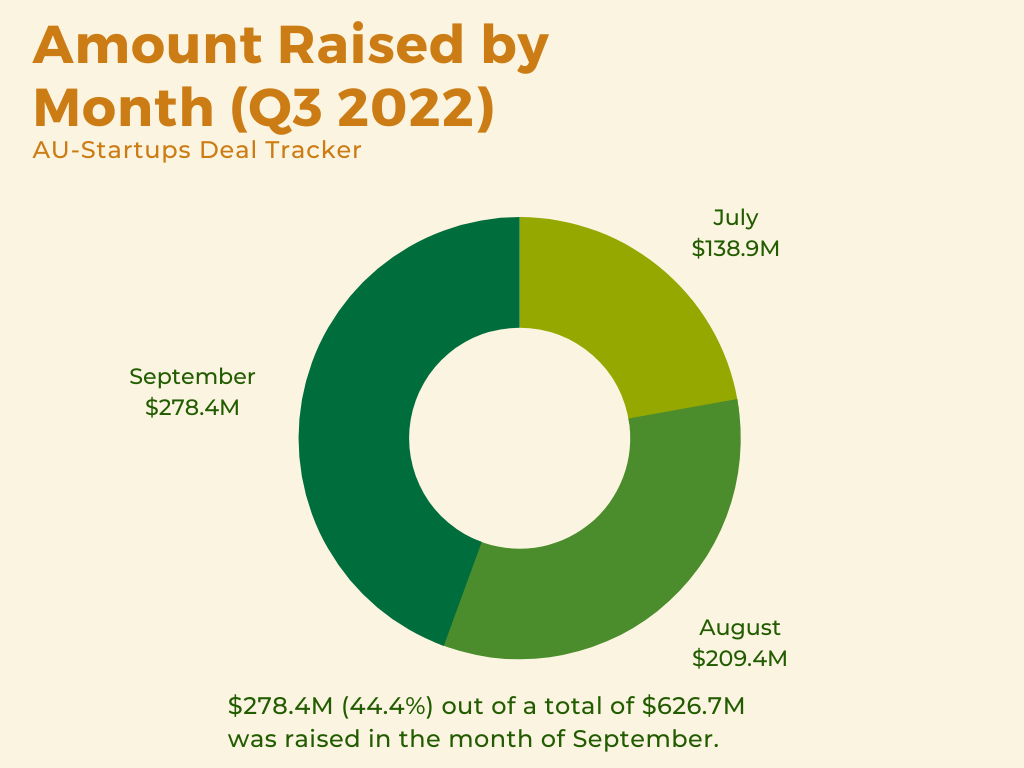

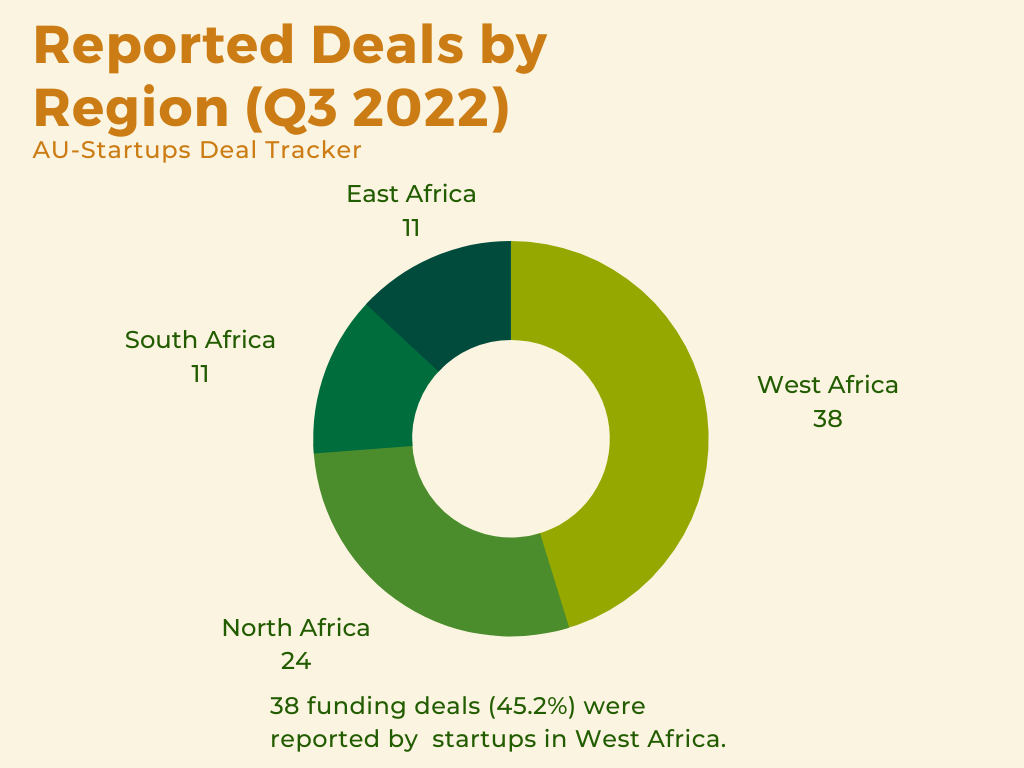

Overall, African startups raised a total of $626.7 million in 84 funding rounds in Q3 2022, with seed rounds being the most popular deal type and Series A being the most valuable deal type overall. West Africa saw the most deals and the highest amount of money invested in startups, largely due to strong performance from Nigerian startups. Fintech was the most heavily invested sector in terms of deal volume, while logistics was the second most-funded sector in terms of deal value.

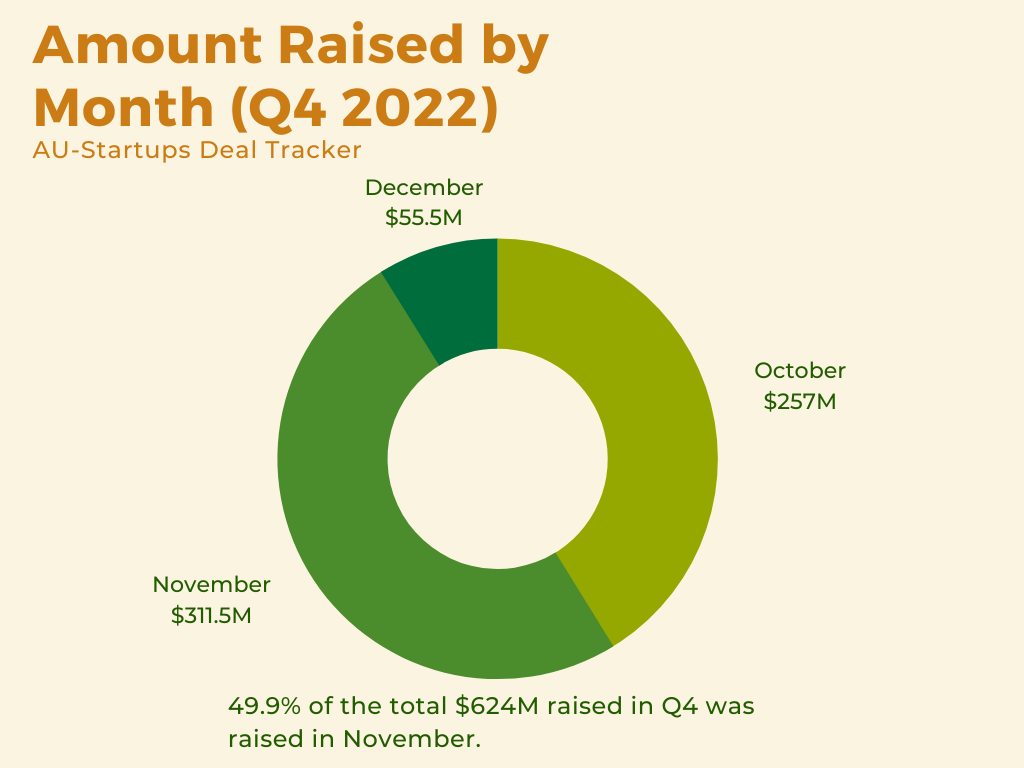

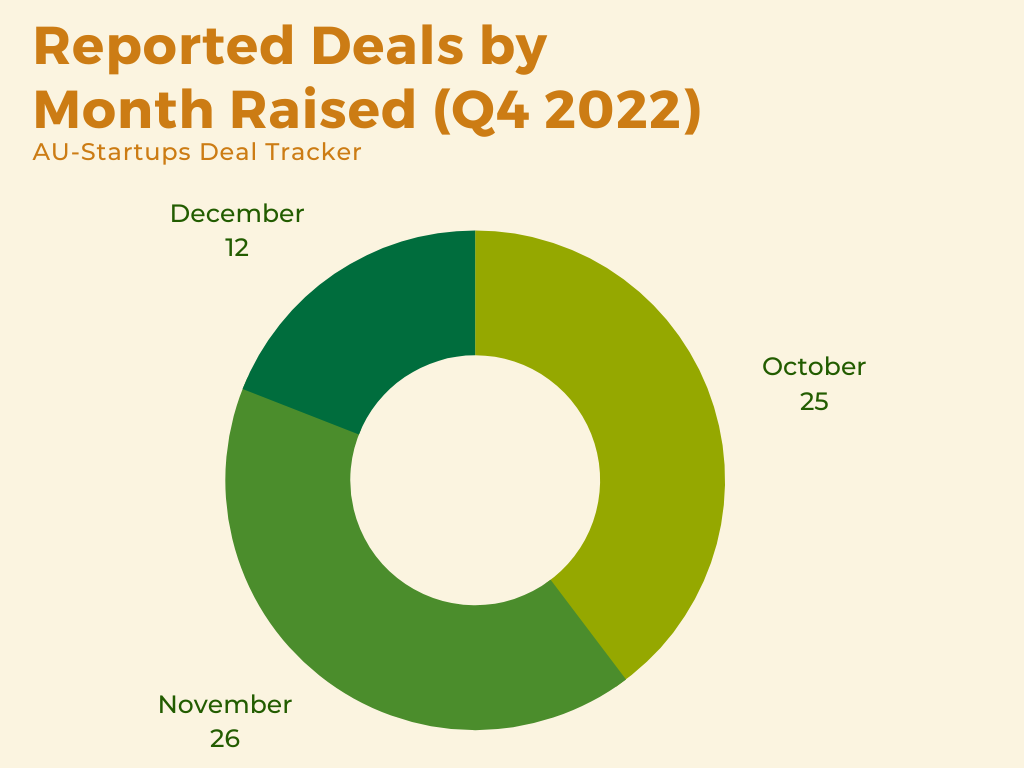

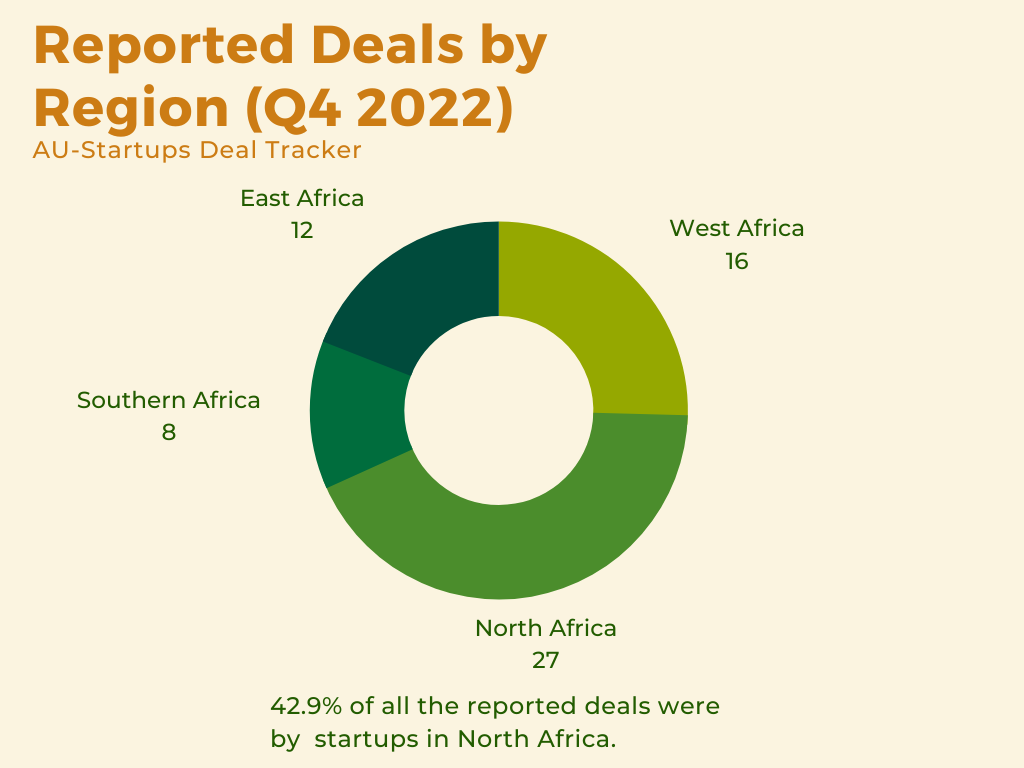

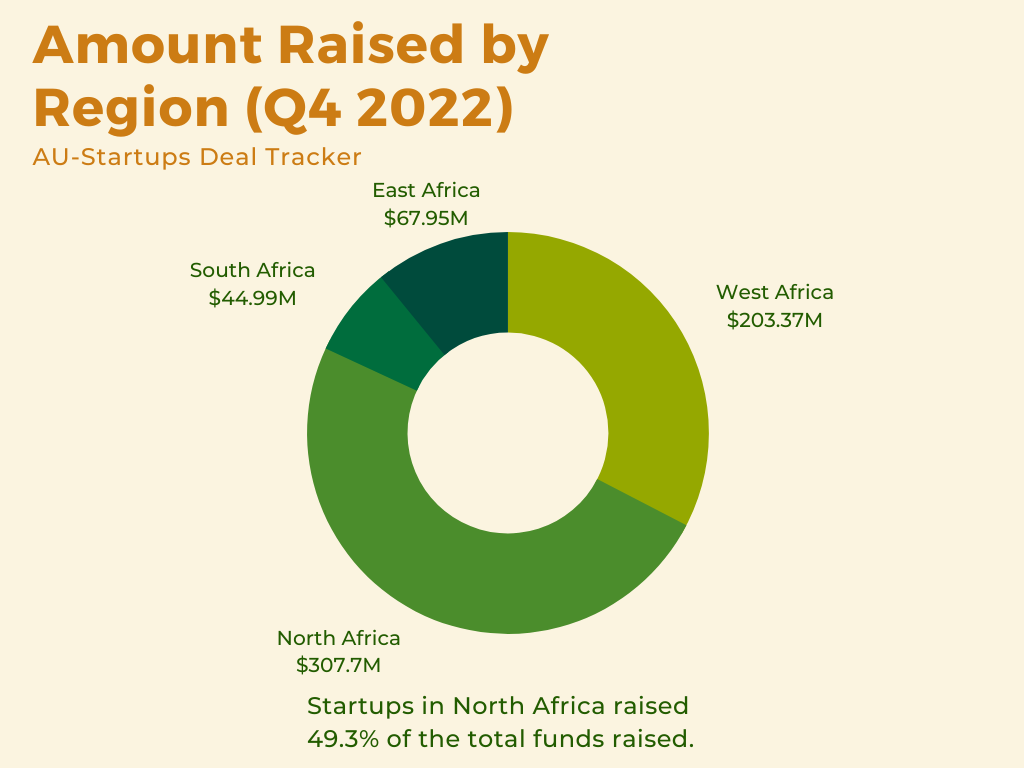

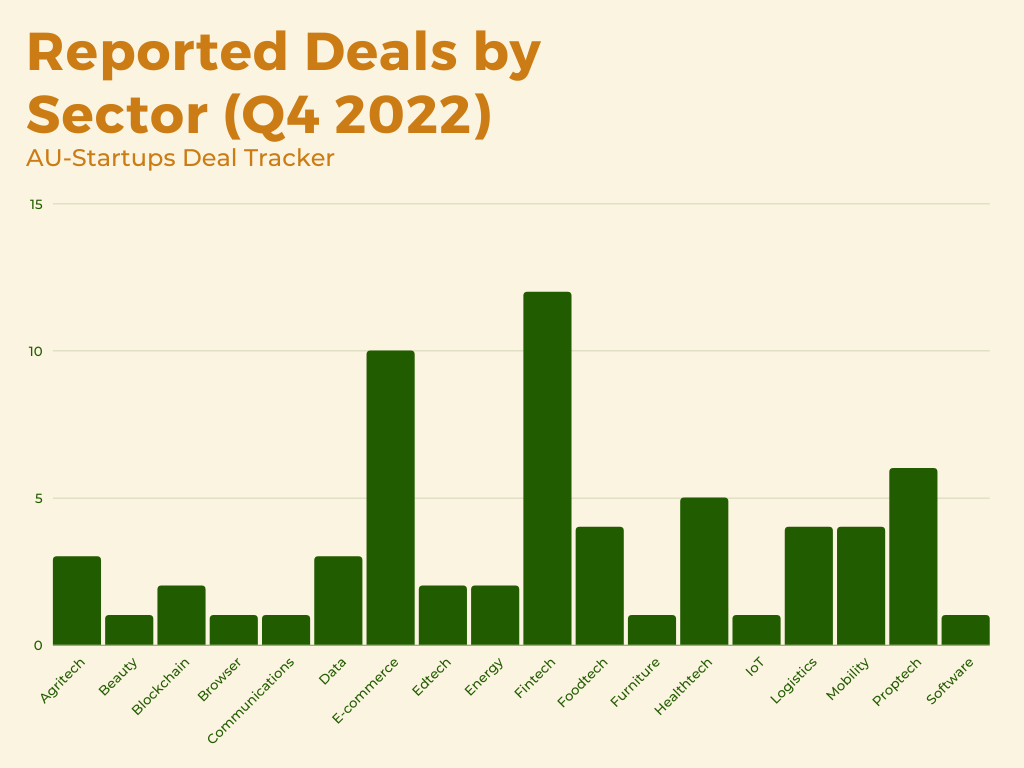

In Q4, there was a 25% decrease in deal volume compared to Q3, but only a 0.43% decrease in the total amount raised. It should be noted that the data collection for Q4 ended on December 9, 2022, so the total amount raised by African startups in Q4 will likely exceed that of Q3. North Africa had the highest deal volume and the highest total amount invested in its startups in Q4, with fintech and logistics being the most funded sectors in terms of deal volume and deal value, respectively.

Q3 & Q4 2022 Key Highlights

In Q3 2022, there were 94 total deals with 84 being disclosed. The top deal was Wave, which received $90 million in debt financing. The top pre-seed deal was Mazaya, which received $5 million from Raya Trade & Distribution. The top seed deal was NowNow, which received $13 million.

The top Series A deal was Vendease, which received $30 million from Partech Africa and TLcom. The top Series B deal was Kobo360, which received $38 million from FEDA, TLcom Capital, IFC, and Juven. The top Series C deal was TeamApt, which received $50 million from QED Pre-Series C. The top VC investor by deal volume was Y Combinator, with 7 deals.

In Q4 2022 however, there were 73 total deals with 64 of them being disclosed. The top deal was a Series B round for Yassir, which raised $150 million. The top pre-seed deal was for Leta, which raised $3 million, and the top seed deal was for Telda, which raised $20 million.

The top Series A deal was for Phoenix Browser, which raised $100 million. The top VC investor was BOND, who led the investment in Yassir and had the highest deal value.

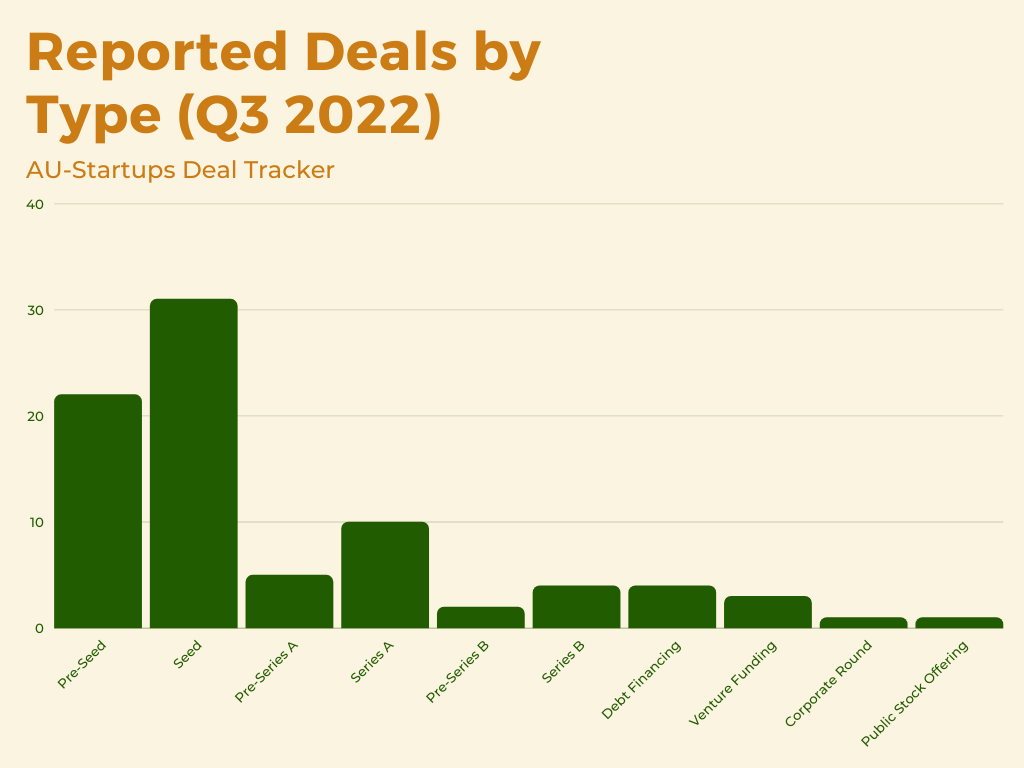

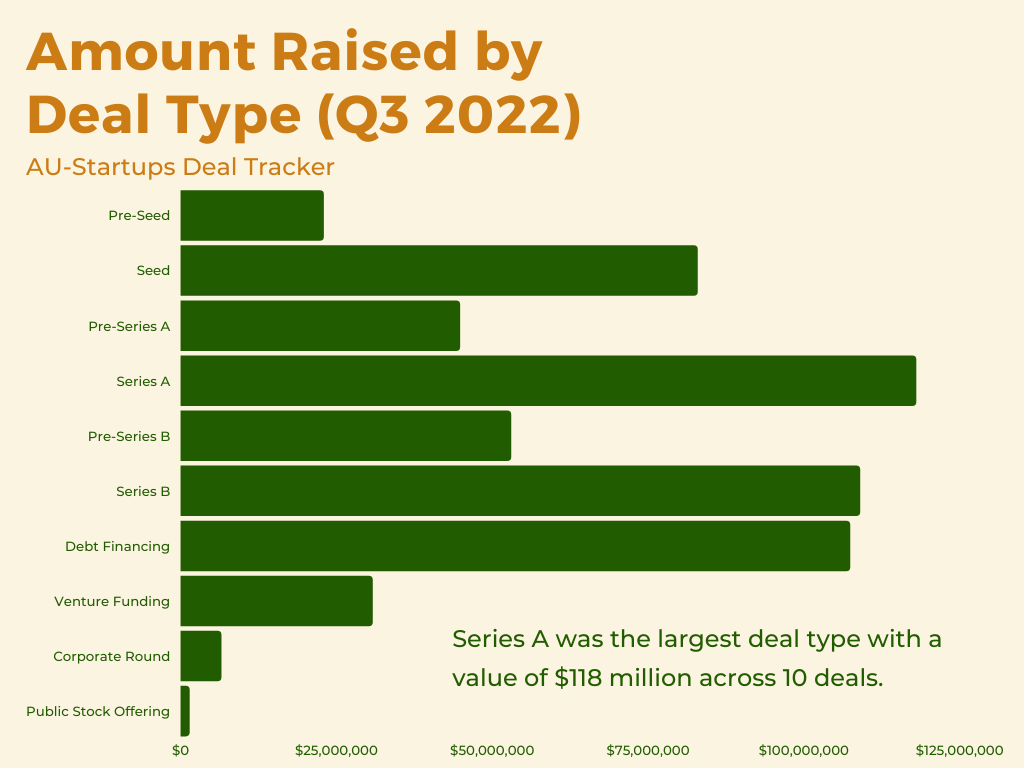

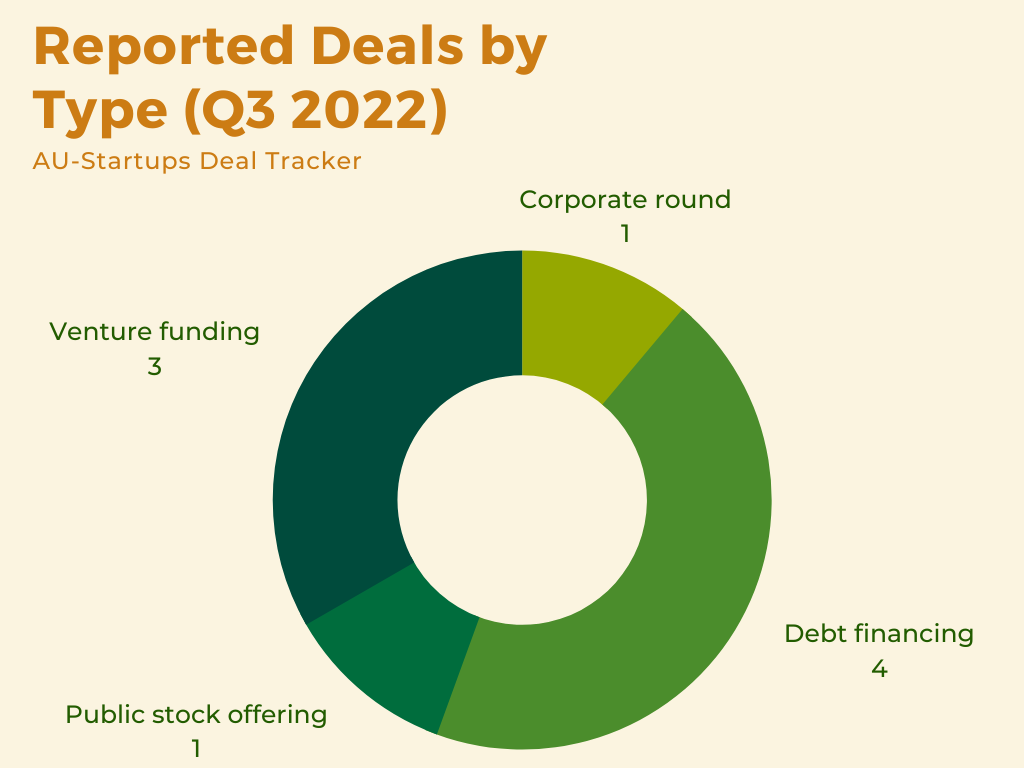

Summary: Q3 2022 Deals by Startup Stages and Volume

Seed rounds were the most popular type of deal, with 31 rounds raising a total of $89.9 million. Pre-seed rounds were the second most popular with 22 deals worth $22.9 million. The largest deal type was Series A, with 10 deals totaling $118 million, followed by Series B with 4 deals worth $109 million.

Pre-Seed

In the third quarter of 2022, the total value of pre-seed funding deals in AU-Startups was $22,931,000 with 22 deals being made. The most active sector was fintech in terms of deal volume and e-commerce in terms of deal value.

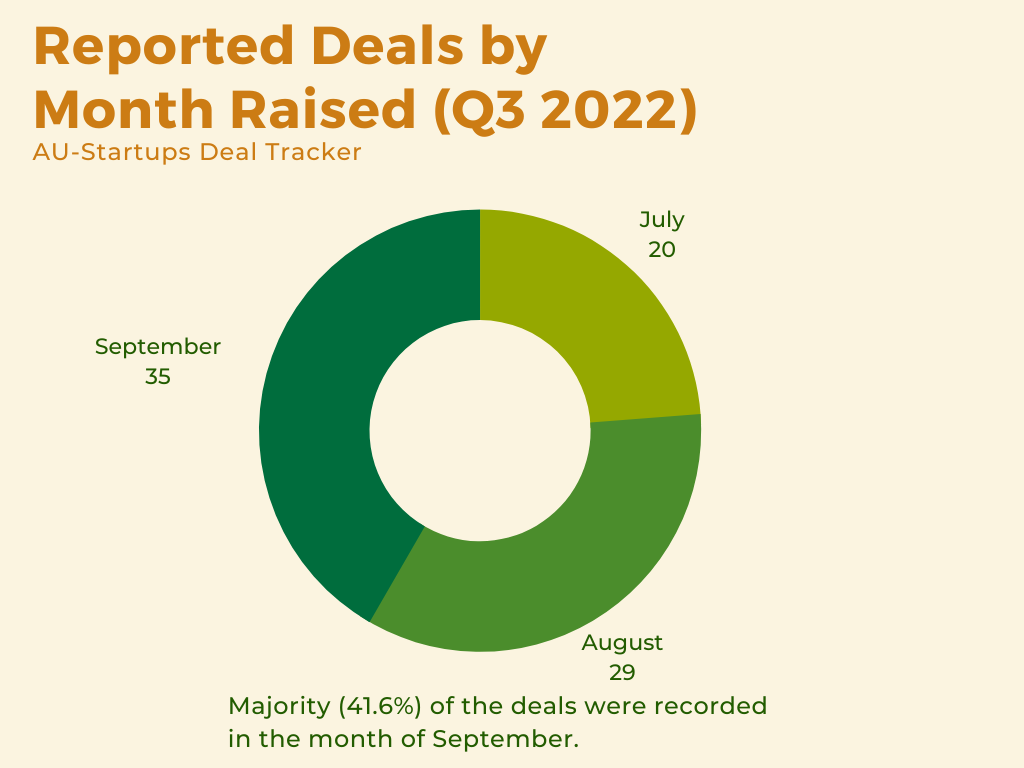

The biggest investor was Raya Trade & Distribution with a $5m investment. Most of the deals took place in Nigeria (9) and Egypt (7). Of the total deals made in Q3, 12 (54.5%) occurred in September.

Seed

In the third quarter of 2022, there were 31 seed funding deals worth a total of $82,929,000. The most active sector was fintech, with 10 (32.6%) of the deals being in this area. The most active countries were Nigeria, Egypt, and Kenya, with 15, 6, and 4 deals respectively.

Pre-Series A

In the third quarter of 2022, five pre-series A funding deals were completed with a total value of $44,800,000. The most active sector was fintech and the biggest investor was Serena Ventures, which invested $12.3 million. The deals were evenly distributed among countries. There were no pre-series A deals raised in July.

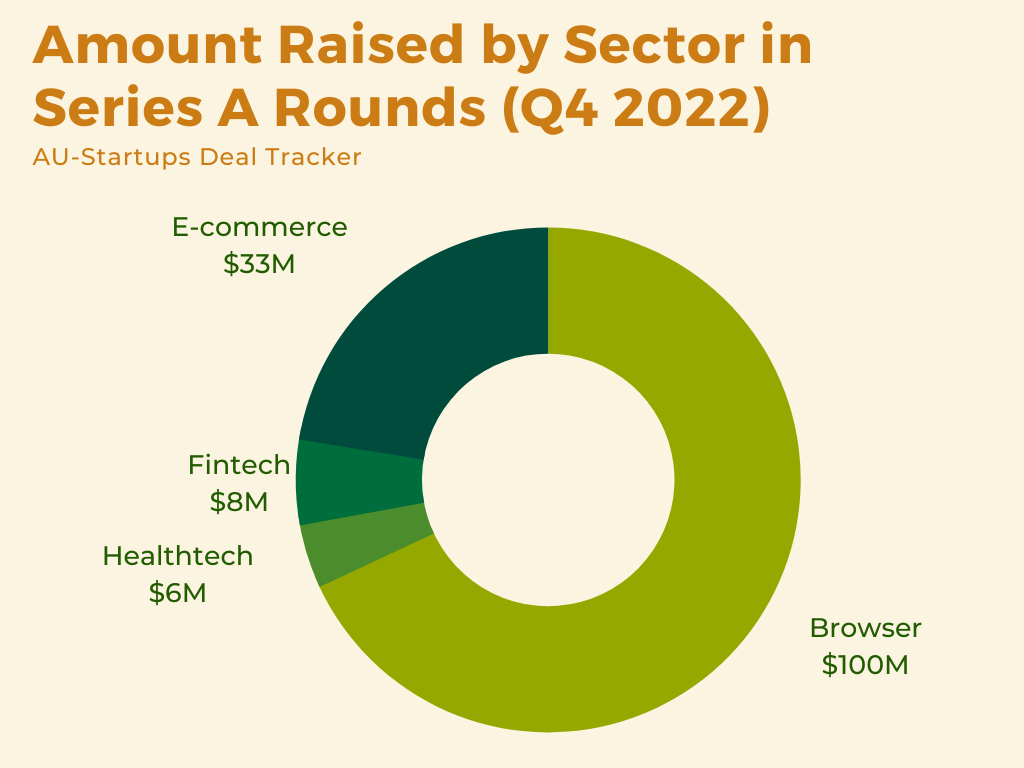

Series A

In Q3 2022, there were a total of 10 Series A funding deals worth $118 million in the AU-Startups ecosystem. The most active sector was e-commerce, and the biggest investor was Knife Capital. The most active countries were South Africa. Additionally, 60% of all Series A deals in this quarter were raised in September.

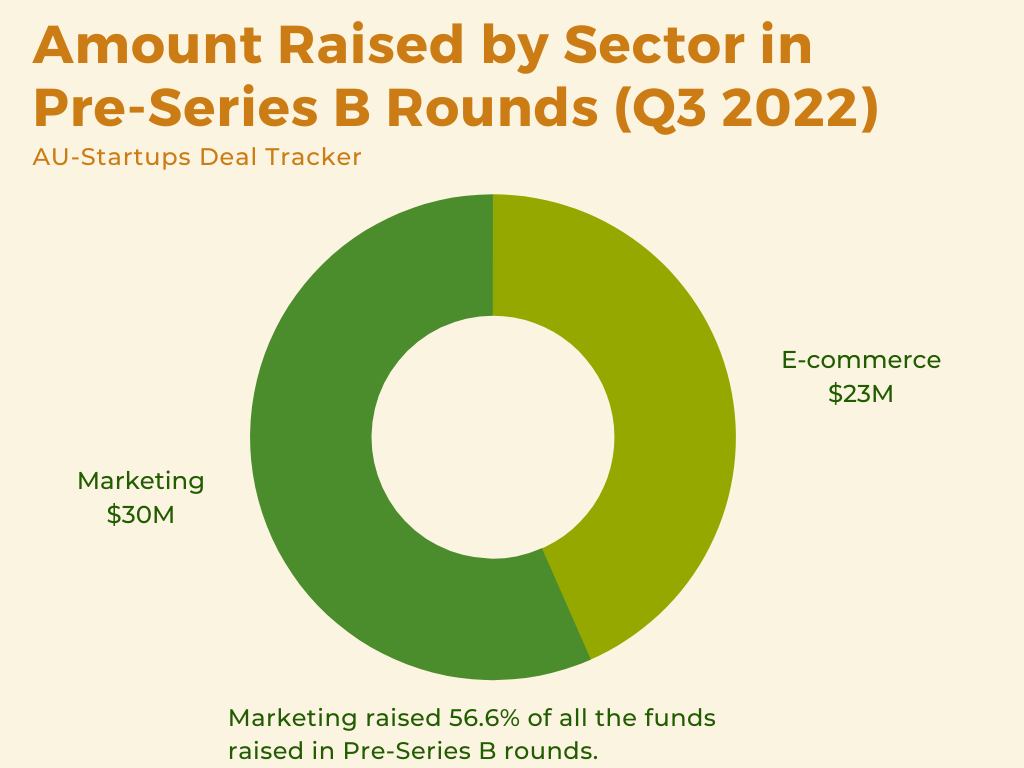

Pre-Series B

In Q3 2022, the AU-Startups Pre-Series B Funding Review saw a total of 2 deals worth $53 million. The sector distribution was even and the biggest investor was AfricInvest. Both deals were in South African startups.

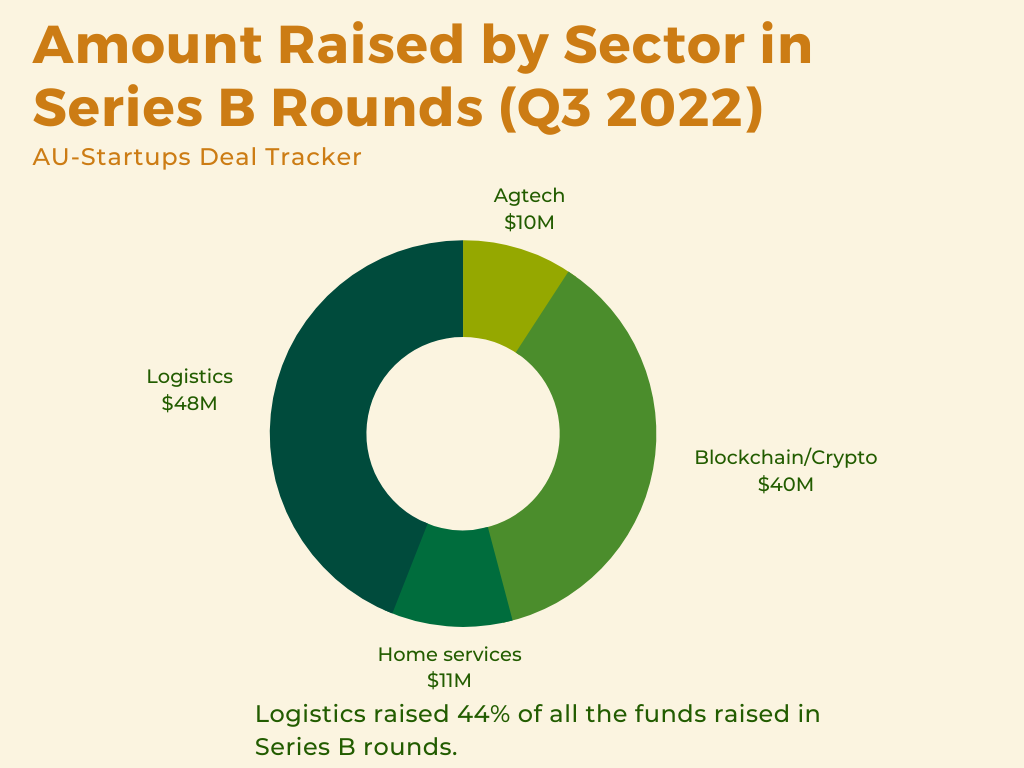

Series B

The AU-Startups Q3 2022 Series B Funding Review showed a total value of $109 million across 4 deals. There was no dominant sector in terms of deal activity and the biggest investor was FEDA. The most active country was Nigeria, with 3 out of 4 of the Series B deals taking place in September.

Pre-Series C

Q3 2022 saw a relatively slow quarter for Series B investments, with only one deal taking place. The total value of this deal was $50 million, and it was in the fintech sector. QED was the biggest investor in this round, and the funding was most active in Nigeria.

The standout deal of the quarter was TeamApt’s funding round, which was led by QED and also included participation from Novastar Ventures, Lightrock, and BII. Overall, it seems that the Series B funding market was somewhat subdued in Q3 2022, with only a single, significant deal taking place.

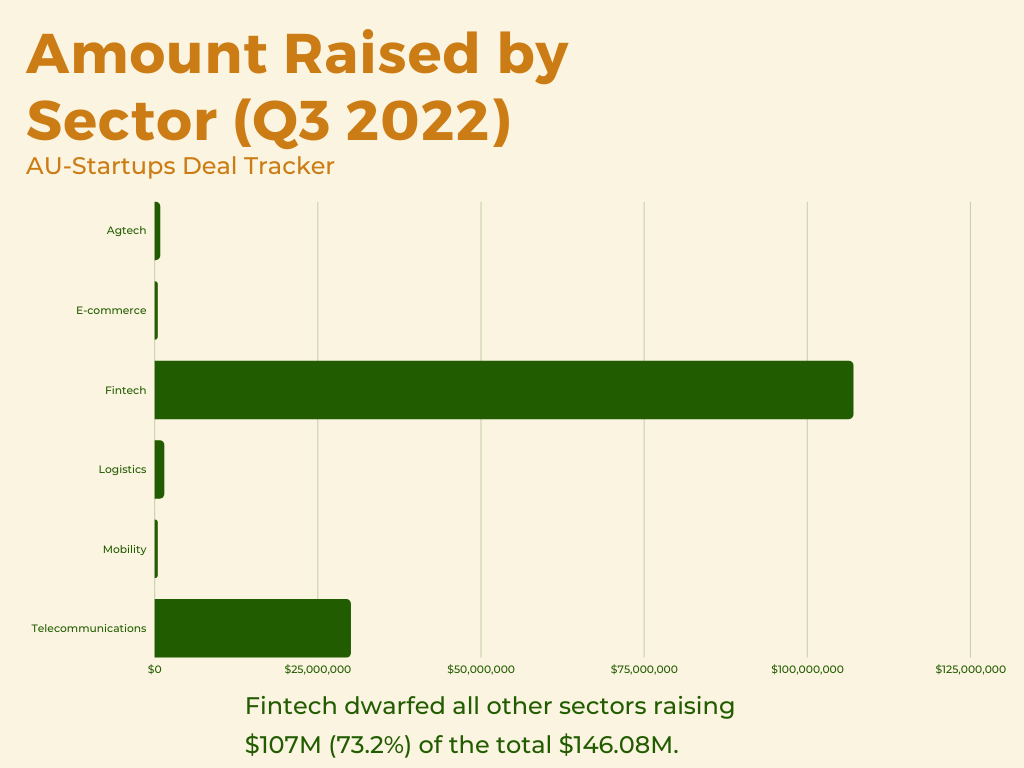

Other deals

In Q3 2022, there were a total of 9 other investment deals in the AU-Startups market, with a total value of $146.1 million. The most active sector for these investments was fintech, and the biggest investor was IFC. South Africa and Ghana were the most active countries, each with 2 deals.

The standout aspect of these investments was the involvement of IFC, which invested a total of $120 million in the two largest deals. Overall, it seems that other investments in the AU-Startups market were fairly active in Q3 2022, with a diverse range of sectors and countries represented.

Summary: Q4 2022 Deals by funding type, region, sector, and value

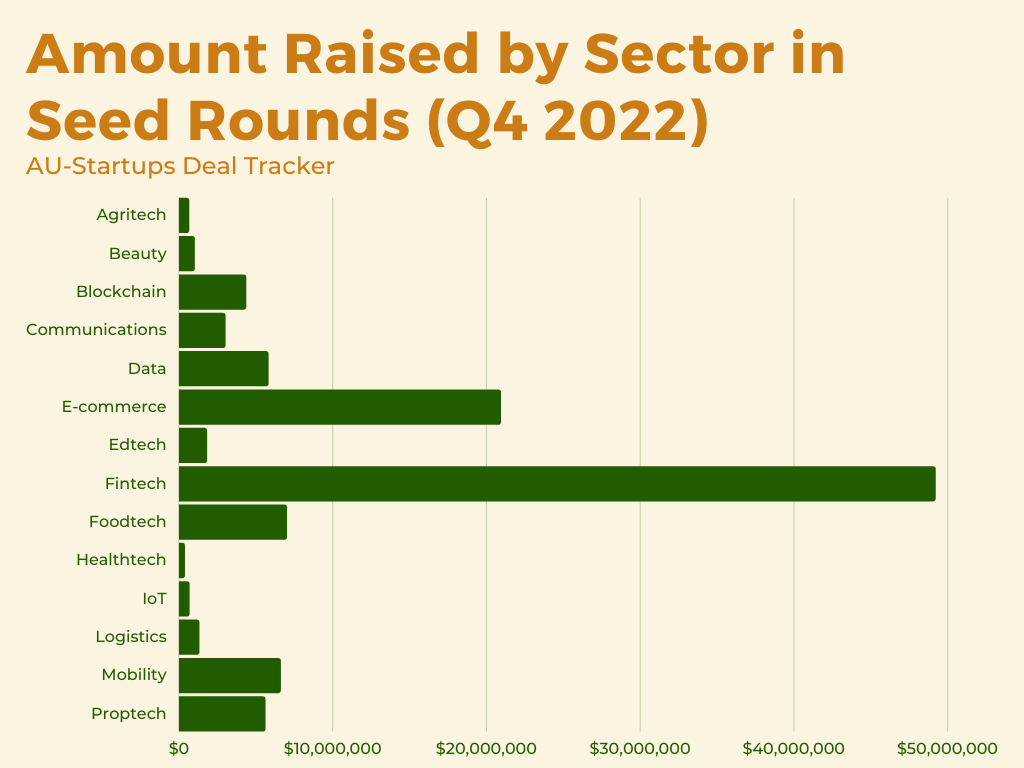

In Q4 2022, according to the data available, seed rounds were the most popular type of deal, comprising 47% of all deals and raising a total of $108.23 million. Pre-seed rounds were the next most common, accounting for 15.6% of deals and raising a total of $12.21 million.

In terms of deal value, Series B rounds raised the most, with a total of $218.5 million raised across 4 deals. Series A rounds were also significant, raising $147 million across 5 deals. Overall, there was a diverse range of funding activity in the AU-Startups market in Africa during this time period, with a mix of deal types and values.

Pre-seed

The fourth quarter of 2022 saw a total of 11 pre-seed funding deals, with a total value of $12.2 million. The most active sector for this funding was proptech, with 4 deals. The biggest investor, based on deal volume, was Plug & Play, which participated in 2 deals. The most active countries for this funding were Egypt and Kenya, with 4 and 3 deals respectively.

A significant proportion of these deals (54.5%) took place in November. Overall, it seems that the pre-seed funding market was fairly active in Q4 2022, with a diverse range of deals across a number of sectors and countries.

Seed

During Q4 2022, the seed funding market in AU-Startups was active, with a total of 30 deals worth $108.2 million. The most active sector for seed funding was fintech, with 7 deals, followed by Egypt and Nigeria with 11 and 7 deals, respectively.

The biggest investor in seed funding during this period was Global Founders Capital, which led the investment in Telda’s round with $20 million. Seed funding rounds were the most frequent type of deal in Q4 2022, and they also contributed 17.3% of the total amount raised during this period.

Pre-Series A

The fourth quarter of 2022 saw only one pre-Series A funding deal, with a total value of $3 million. The deal was in the health-tech sector and involved Lifestores Healthcare in Nigeria. From the data available it appears that the pre-Series A funding market was relatively quiet in Q4 2022, with only a single, or small deal taking place.

Series A

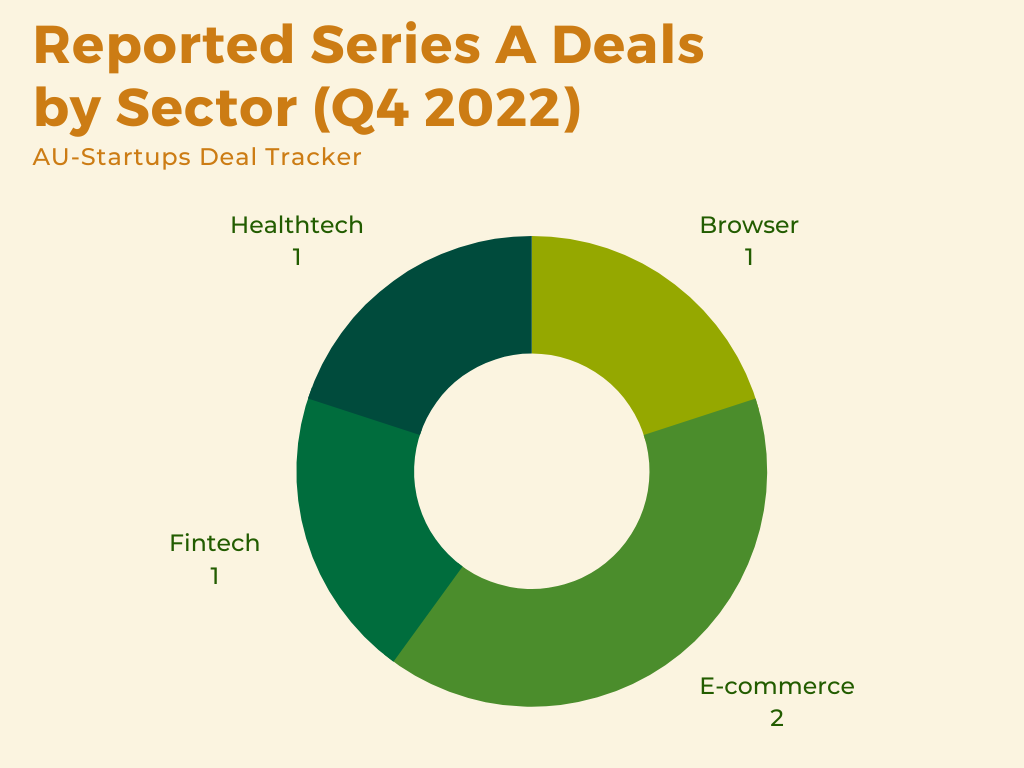

In Q4 2022, there were a total of 5 Series A funding deals, with a total value of $147 million. The most active sector was e-commerce, with 2 deals in this sector. The biggest investor in this round were Flexcap Ventures and Jared Schreiber, who invested $32 million in the biggest deal. The investors in the biggest round, which was worth $100 million, were not disclosed.

The most active countries for this funding were Nigeria, with 2 deals. Overall, Series A funding made up 7.9% of the total deal volume in Q4 2022 but contributed significantly to the total deal value at 23.6%.

Pre-Series B

In Q4 2022, there was only one Pre-Series B funding deal that took place, with a total value of $40 million. This funding was for the Egyptian e-commerce startup MaxAB, and the deal was worth $40 million. Overall, it appears that the Pre-Series B funding market was relatively quiet in Q4 2022, with only one deal taking place.

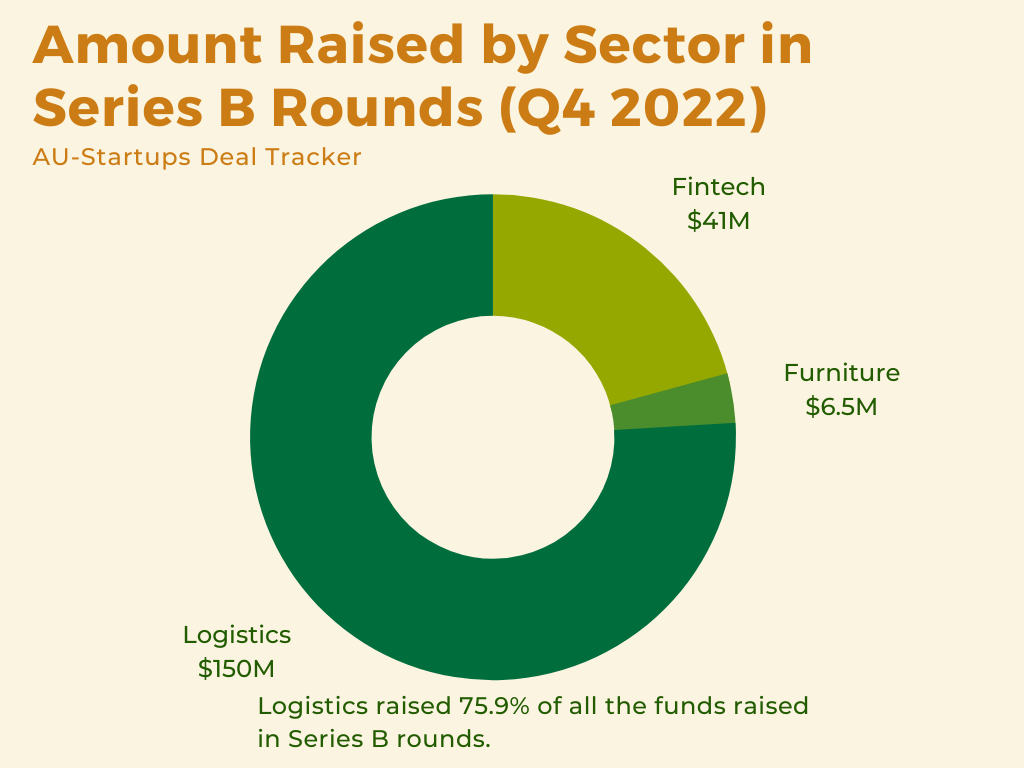

Series B

Q4 2022 saw an increase in activity in the Series B funding market, with a total value of $187.5 million across three deals. The most active sector was evenly distributed among various industries, and the biggest investor was BOND, which led a $150 million deal as the lead investor.

The most active countries for this funding were also evenly distributed. Series B rounds were the most common type of deal in Q4 2022, with the largest deal of the quarter being a Series B round led by BOND. Overall, it seems that the Series B funding market picked up in Q4 2022, with multiple significant deals taking place.

Other Deals

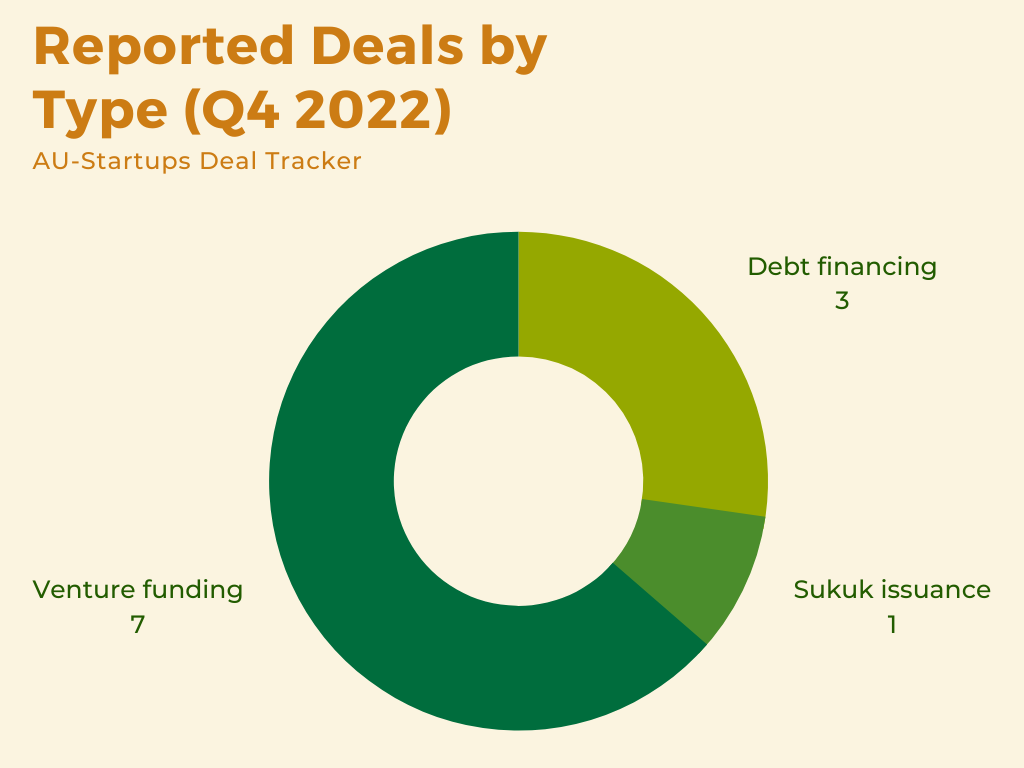

The AU-Startups Q4 2022 Series B Funding Review showed that there were a total of 12 funding deals in the quarter, with a total value of $126 million. The most active sectors were fintech and mobility, with three deals each. Franklin Templeton Investments was the biggest investor in this round, with a $30 million sukuk issuance as the sole investor in Moove.

The most active countries for this funding were Egypt, with four deals, and Nigeria and South Africa, with two deals each. Debt financing was the most valuable deal type, accounting for $72.1 million of the total value of deals. Overall, the Series B funding market in Q4 2022 was active, with a diverse range of sectors and countries represented.

Conclusion

African startups saw a 25% decrease in deal volume in Q4 2022, but only a 0.43% decrease in total funding compared to Q3 2022. The fintech sector experienced a 46.2% decrease in funding between Q3 and Q4, while the logistics sector saw an impressive 89.5% increase in funding. The mobility sector also saw significant growth, with a 3,857% increase in funding between Q3 and Q4. E-commerce saw a 37.6% decrease in funding.

In terms of deal types, seed rounds were the most popular in Q3 2022, while Series A was the most valuable deal type overall. West Africa saw the most deals and the highest amount of money invested in startups, largely due to strong performance from Nigerian startups. Fintech was the most heavily invested sector in terms of deal volume, while logistics was the second most-funded sector in terms of deal value.

Source: dealtable.au-startups.com

*Note: Data collection for Q4 ended on Friday, December 9, 2022

Comments 1